A new milestone for science at NTU: The inauguration of the Max Planck-IAS-NTU Center

瀏覽器版本過舊,或未開啟 javascript

請更新瀏覽器或啟用 javascript

Spotlights

Date: Aug 11, 2021

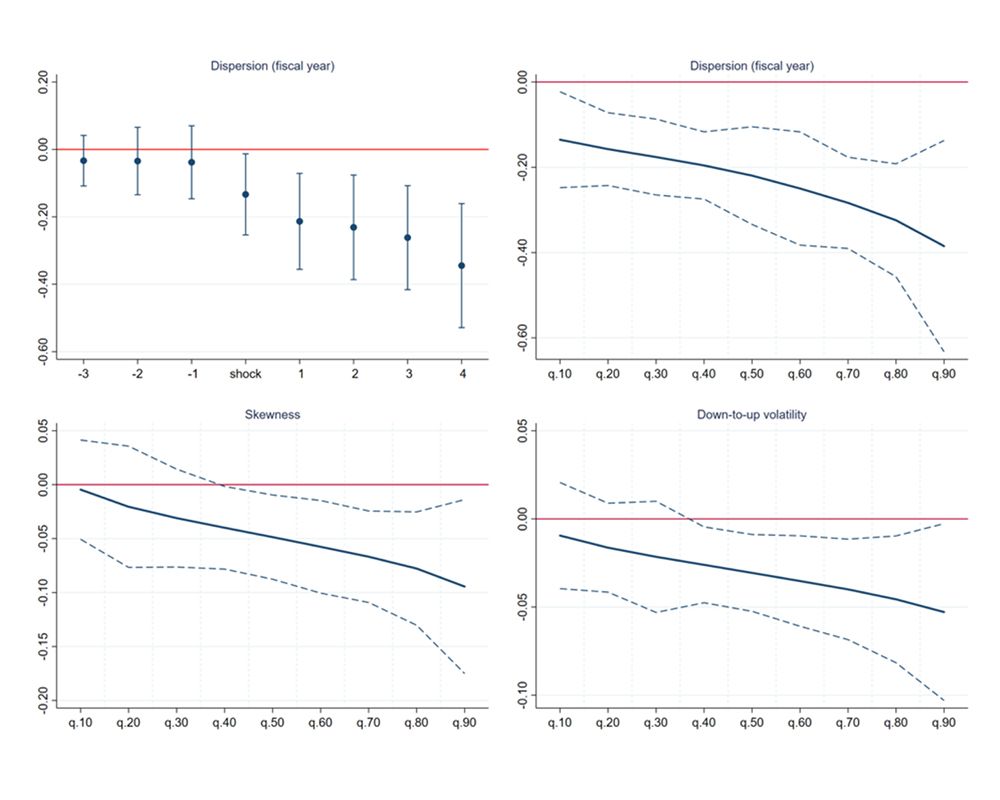

Investor disagreement dynamics and quantile regressions.

The research team.

Testing Disagreement Models, new research by NTU Department of Finance faculty Yen-Cheng Chang (張晏誠) and Kevin Tseng (曾俊凱), doctoral student Pei-Jie Hsiao (蕭珮婕) and Stockholm School of Economics faculty Alexander Ljungqivst is forthcoming in The Journal of Finance, marking the first acceptance of NTU scholars by the journal since 1999.

Asset pricing is a core field in financial economics. One of the major challenges of asset pricing is to propose models that can explain the behavior of asset prices. In this regard, models that incorporate investor disagreement can be used to explain empirical regularities such as investor overtrading, asset bubbles, and stock price crashes. These are all issues of great interest to academics, practitioners, and policy makers. While models of investor disagreement are appealing on theoretical grounds, prior empirical studies fall short of providing causal evidence for the role of disagreement in asset prices.

The main innovation in the new research is to exploit a regulation in the 1990s by the Securities and Exchange Commission (SEC) requiring all public firms to submit and disclose their financial reports online. The research team uses this empirical setting as a natural experiment and finds that this regulation induces a reduction in investor disagreement, which in turn alleviates speculative stock price bubbles and crash risks. The team also finds that these effects are more pronounced for stocks with binding short-sale constraints, which is consistent with models of investor disagreement. Overall, this research uses a single identification strategy to test all core predictions of disagreement models, thus establishing causal relations between investor disagreement and important asset pricing phenomena. This contribution is key in receiving recognition from the world’s leading academic outlet in finance: The Journal of Finance.

The research idea was originated during the 2017 FMA Asia Pacific Conference hosted by the NTU Department of Finance, where Dr. Chang, Dr. Tseng and Dr. Ljungqvist, an NYU professor at the time, engaged in productive discussions regarding this project. Later they formed a research team and started to work tirelessly in the subsequent years, meeting virtually and physically in the U.S., Europe, and Taiwan.

Dr. Chang and Dr. Tseng would like to extend their gratitude to the College of Management and the Department of Finance at NTU. Their appreciation also goes to the Center for Research in Econometric Theory and Applications (CRETA), Ministry of Science and Technology, and the Higher Education Sprout Project hosted by the Ministry of Education. Both researchers are thrilled to share their latest research results with the academic community throughout Taiwan and the globe.

Testing Disagreement Models

Please refer to the published paper for details on the results of the study:

https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3489666

This study is accepted by The Journal of Finance on July 20th, 2021.

A new milestone for science at NTU: The inauguration of the Max Planck-IAS-NTU Center

A Distinguished Global Research Center Established at NTU under Trilateral Cooperation

Collaborative study between NTU and Japan uncovers the origin of Adzuki Beans and agriculture in Japan

NTU Launches Center for Innovation in Enterprise Law—with Forum Highlighting Trump’s Policy and Legal Shifts Amid Geopolitical Tensions

NTU and Ministry of Environment Sign MOU to Advance Net-Zero Transition and Environmental Resilience

Current Spotlights

A new milestone for science at NTU: The inauguration of the Max Planck-IAS-NTU Center

A Distinguished Global Research Center Established at NTU under Trilateral Cooperation

Collaborative study between NTU and Japan uncovers the origin of Adzuki Beans and agriculture in Japan

NTU Launches Center for Innovation in Enterprise Law—with Forum Highlighting Trump’s Policy and Legal Shifts Amid Geopolitical Tensions

NTU and Ministry of Environment Sign MOU to Advance Net-Zero Transition and Environmental Resilience